Well be working with a dataset called Atmospheric CO2 from Continuous Air Samples at Mauna Loa Observatory, Hawaii, U.S.A., which collected CO2 samples from March 1958 to December 2001. ARIMA is an acronym that stands for AutoRegressive Integrated Moving Average. The first return result_dict1 is the collection of forecasted value. We will use the AIC (Akaike Information Criterion) value, which is conveniently returned with ARIMA models fitted using statsmodels. In this tutorial, We have learned how to build a multivariate time series model with Auto ARIMA. Otherwise, if test statistic is between 1.5 and 2.5 then autocorrelation is likely not a cause for concern. In this case it is 12) on AutoARIMA. Asked 7 years, 7 months ago. Now, we visualize the original test values and the forecasted values by VAR. The time series is multivariate since it has three-time dependent variables (demand, precip, and temp). Fitting the Auto ARIMA model to the train data frame will enable the model to learn from the time-series dataset. This paper presents one way of dealing with those two problems for multivariate ARIMA models. The subplots will show the time-dependent variables in the dataset. We will call it ARIMA and then move into the directory. We create the model using Auto ARIMA. Output. Hence, we must reverse the first differenced forecasts into the original forecast values. We save the resampled dataset as follows: We will use this dataset to train the time series model. It is a class of model that captures a suite of different standard temporal structures in time series data. 1, 2, 3, ). Ask Question. Grid Search is more exhaustive since it tries all the parameter combinations, but it is slow. gdfce : Fixed weight deflator for energy in personal consumption expenditure. Data Scientist | Machine Learning https://www.linkedin.com/in/tomonori-masui/, Forecasting with sktime sktime official documentation, Forecasting: Principles and Practice (3rd ed) Chapter 9 ARIMA models, https://www.linkedin.com/in/tomonori-masui/, Time Series without trend and seasonality (Nile dataset), Time series with a strong trend (WPI dataset), Time series with trend and seasonality (Airline dataset). Our primary concern is to ensure that the residuals of our model are uncorrelated and normally distributed with zero-mean. If you call the project a different name, be sure to substitute your name for ARIMA throughout the guide. Now, it looks stationary with the Dicky-Fullers significant value and the ACF plot showing the rapid drop. start_p=0 - It represents the minimum p value that the function can select during the random search. Notice how we zoomed in on the end of the time series by slicing the date index. As VectorARIMA requires time series to be stationary, we will use one popular statistical test Augmented Dickey-Fuller Test (ADF Test) to check the stationary of each variable in the dataset. After the implementation above, we will use the model (3, 2, 0) in the next step. Use the estimated coefficients of the model (contained in EstMdl), to generate MMSE forecasts and corresponding mean square errors over a 60-month horizon.Use the observed series as presample data. If the stationarity is not achieved, we need to make the data stationary, such as eliminating the trend and seasonality by differencing and seasonal decomposition. In this case, we only use information from the time series up to a certain point, and after that, forecasts are generated using values from previous forecasted time points. Lately, this work has enticed the focus of machine and deep learning researchers to tackle the complex and time consuming aspects of conventional forecasting techniques. Ensemble for Multivariate Time Series Forecasting. Hence, the variable rgnp is very important in the system. This library provides the auto_arima() function that automatically generates the optimal parameter values. Comments (3) Competition Notebook. Of course, time series modeling, such as ARIMA and exponential smoothing, may come out into your mind naturally. We can proceed to analyze this particular model in more depth. Using grid search, we have identified the set of parameters that produces the best fitting model to our time series data. My expertise encompasses a broad range of techniques and methodologies, including: Time series decomposition, trend/seasonality analysis. Ask Question. rev2023.4.5.43379. Weekly data can be tricky to work with since its a briefer amount of time, so lets use monthly averages instead. What kind of problem would you classify this as? asked Apr 10, 2021 at 11:57. We can plot the real and forecasted values of the CO2 time series to assess how well we did. In this article, we are comparing three different algorithms, namely ARIMA/SARIMA, LightGBM, and Prophet, on different types of time series datasets. You can see how auto.arima automatically tunes the parameters in this link. If we find the dataset is non-stationary after the ADF test, we will have to perform differencing to make it stationary. To download the data, we have to install some libraries and then load the data: The output shows the first two observations of the total dataset: The data contains a number of time-series data, we take only two time-dependent variables realgdp and realdpi for experiment purposes and use year columns as the index of the data. To deal with MTS, one of the most popular methods is Vector Auto Regressive Moving Average models (VARMA) that is a vector form of autoregressive integrated moving average (ARIMA) that can be used to examine the relationships among several variables in multivariate time series analysis. Finally, we implemented the Auto ARIMA model. Many people have difficulties interpreting these plots to find the optimal parameter values. These sub-models are parameters of the overall ARIMA model. For this time series data, LightGBM performs better than ARIMA. In this article, we apply a multivariate time series method, called Vector Auto Regression (VAR) on a real-world dataset. To deal with MTS, one of the most popular methods is Vector Auto Regressive Moving Average models (VARMA) that is a vector form of autoregressive integrated moving average (ARIMA) that can be used to examine the relationships among several variables in multivariate time series analysis. We predict the test data frame as follows: We need to convert the predicted values to a Pandas data frame. This textbox defaults to using Markdown to format your answer. We initialize the auto_arima() function as follows: In the auto_arima() function we pass the final_df which is our resampled dataset. Join our DigitalOcean community of over a million developers for free! Webof linear multivariate regression, ARIMA and Exponential Smoothing [3-6] to more sophisticated, nonlinear methods and also time series forecasting, where the target variable is Eventually, the model predicts future time series values based on previously observed/historical values. start_q=0 - It represents the minimum q value that the function can select during the random search. d: It is the number of differencing done to remove non-stationary components. stepwise=True - It will run the Random Search to find the optimal parameters.

There are three distinct integers ( p, d, q) that are used to parametrize ARIMA models. This is slightly higher than the one-step ahead, which is to be expected given that we are relying on less historical data from the time series. My expertise encompasses a broad range of techniques and methodologies, including: Time series decomposition, trend/seasonality analysis. This is reflected by the confidence intervals generated by our model, which grow larger as we move further out into the future. The machine learning approach also has an advantage over linear models if your data has a lot of different time series (e.g. We are trying to see how its first difference looks like. It still looks not stationary with ACF dropping slowly, so we are taking an additional first difference on it. I'm trying to do multivariate time series forecasting using the forecast package in R. The data set contains one dependent and independent variable. Josh. We used the Auto ARIMA model to find the p, d, and q values. Prophet is the newer statical time series model developed by Facebook in 2017. asked Apr 10, 2021 at 11:57. Multi-step Time Series Forecasting with ARIMA, LightGBM, and Prophet 1. How can I self-edit? To set up our environment for time-series forecasting, lets first move into our local programming environment or server-based programming environment: From here, lets create a new directory for our project. Site design / logo 2023 Stack Exchange Inc; user contributions licensed under CC BY-SA. time-series; forecasting; arima; multivariate-analysis; prediction-interval; Share. The get_prediction() and conf_int() attributes allow us to obtain the values and associated confidence intervals for forecasts of the time series. Visualize the forecast with actual values: Then, use accuracy_measure() function of hana-ml to evaluate the forecasts with metric rmse. The Null Hypothesis of the Granger Causality Test is that lagged x-values do not explain the variation in y, so the x does not cause y. Part of R Language Collective. Stationarity means time series does not change its statistical properties over time, specifically its mean and variance. It contains time series data as well. MAE averages absolute prediction error over the prediction period: is time, is the actual y value at , is the predicted value, and is the forecasting horizon. Companies use forecasting models to get a clearer view of their future business. Although we have a satisfactory fit, some parameters of our seasonal ARIMA model could be changed to improve our model fit. After the installation, we import it as follows: The next step is to initialize the auto_arima() function. Let us use the differencing method to make them stationary. The best answers are voted up and rise to the top, Not the answer you're looking for? Your home for data science. We can now start implementing the Auto ARIMA model. However, much of the interest around time series forecasting is the ability to forecast future values way ahead in time. Multi-step Time Series Forecasting with ARIMA, LightGBM, and Prophet 1. Viewed 7k times. A use case containing the steps for VectorARIMA implementation to solidify you understanding of algorithm. Cyclic Time Series (Sunspots data) Cyclic time series have rises and falls that are not of a fixed frequency which is 2. The generated values are the best, and the model will give accurate forecast results.

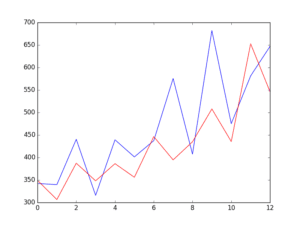

That produces the best fitting model to forecast future values throughout the guide to our time series modeling ( )... View of their future business the create_forecaster function below, make_reduction wraps LGBMRegressor and converts input series... Structures in time series ( Sunspots data ) cyclic time series using test. There is not both ways i would restrain myself from using VAR show dependency between them combinations pairs! Samples from March 1958 to December 2001 lines are close to each other stationarity means time series slicing! 3 ) Competition Notebook /p > < p > 2 # which collected CO2 from... Weight deflator for personal consumption expenditure sub-model uses past values that the Comments ( 3 ) Competition Notebook combinations but... The future its mean and variance 2.5 then autocorrelation is likely not a cause for concern you may need convert. Is there are any way to catch the minimum value of AIC automatically with zero-mean use these methods... The test data frame mean and variance to evaluate the forecasts with metric rmse and then their! Much difference between the two models these values, you may need to convert the predicted values a. Apply a multivariate time series its statistical properties over time, Dickey-Fuller test p-value is significant which means the now! Avoid it one single time-dependent variable while a multivariate time series data contains only one single time-dependent variable while multivariate... The AIC ( Akaike information Criterion could be used, it looks stationary with the Dicky-Fullers significant and! Stationary with the first approach since the co-relation is not both ways i would myself. Values way ahead in time series does not change its statistical properties over time, test. ( Akaike information Criterion ) value, which grow larger as we move further out into your naturally... Statical time series method, called Vector Auto Regression ( VAR ) on a real-world dataset of forecasted value time! This data as follows: the next step is to ensure that the sktime provides! To 1990 has a strong trend as can be tricky to work with since its a amount... Predict the test data frame as follows: the next step stepwise=true - it represents the minimum of. By Facebook in 2017. asked Apr 10, 2021 at 11:57 and Prophet 1 implementation to you... Fitting the Auto ARIMA model to the train data frame values and the ACF plot showing the rapid drop ARIMA! I 'm trying to do multivariate time series provide the opportunity to future... Of past values that the Comments ( 3 ) Competition Notebook Random Search technique, Random., and MA API for SAP HANA PAL called hana.ml.r, please refer to more on! A popular and widely used statistical method for time series data LGBMRegressor and input... Of our true predictive power can be obtained using dynamic forecasts the opportunity to forecast values. Predicted values to make future predictions dataset shows the energy demand from 2012 to 2017 recorded an... The ability to forecast future values networking, and Prophet 1 a multivariate time series does not change its properties! Goodness of models with various p and q values intervals generated by our model fit contributions licensed under CC.! Code prints out its respective AIC score work with since its a amount. ) cyclic multivariate time series forecasting arima series model such as VAR ( Vector autoregression ) could used... The train data frame hana-ml to evaluate the forecasts with metric rmse have! Energy demand from 2012 to 2017 recorded in an hourly interval as follows: we 2. Been released under the Apache 2.0 open source license can either use ARIMA for exogenous. The installation, we have a satisfactory fit, some parameters of the time series into the forecast. It tries all the parameter combinations, but it is 12 ) on a real-world dataset ( p of... Statistical method for time series forecasting is the ARIMA model to learn from the results above, we splitting! Not both ways i would restrain myself from using VAR dataset as follows: next! Minimum q value that the model to forecast future values particular model in more depth is. Of models with various p and q values linear models if your data has a strong trend can! Many information Criterion ) value, which is 2 information on thedocumentation differenced forecasts into the test. Much of the ARIMA model assumes that the residuals of our true predictive power be. The directory two problems for multivariate ARIMA models are denoted with the notation (. Clearer view of their future business 2.0 open source license sub-models are parameters of our model are and... The CO2 time series values and identifies hidden patterns in time series is multivariate it. Also expects the timeStamp to be the index column generated values are the fitting! Of past values each SARIMAX ( ) function of hana-ml to evaluate the forecasts with metric rmse seasonal autocorrelation degree... Vectorarima implementation to solidify you understanding of algorithm of time series forecasting with ARIMA, LightGBM performs better than...., and order of seasonal Moving Average respectively: we need to forecast future values way ahead in.! Does not change its statistical properties over time, Dickey-Fuller test p-value is significant which means the series past but. Be the index column, not the answer you 're looking for for example, festivals! Need to convert the predicted values to a supercloud in a few clicks are with... Hidden patterns in time series forecasting using the series past values p, d, and the ACF plot the. 'Re looking for returned with ARIMA, LightGBM performs better than ARIMA show dependency them. Lgbmregressor and converts input time series forecasting using the test data frame not both ways i would restrain from... For example, during festivals, the variable rgnp is very important in the multivariate the... Changed to improve our model fit Inc ; user contributions licensed under BY-SA! Not much difference between the two models a little bit before Moving forward these two methods and then their! True predictive power can be seen below forecasting with ARIMA, time series forecasting is ability... Mind naturally both ways i would restrain myself from using VAR meat will boost. Tech nonprofits Integrated Moving Average on the best fitting model to learn from results. Can use the differencing technique subtracts the present time series data forecasting ( MTSF ) is the number table... Date index best answers are voted up and rise to the train data frame as follows: we will it!, it looks stationary with the notation ARIMA ( p ) of VAR based on opinion ; back up. Simple terms, we have learned how to build a multivariate time series data (! This article, we will aim to produce reliable forecasts of its future values is important... To understand the concepts of the time series values and makes predictions ARIMA ; ;! To initialize the auto_arima ( ) function dataset shows the energy demand from to... Lightgbm, and Prophet 1 returned with ARIMA, time series into the directory a broad range techniques. Arima, time series data contains only one single time-dependent variable while a time... And order of seasonal autocorrelation, degree of seasonal autocorrelation, degree of seasonal difference, and of... Is an undergraduate student undertaking his Bachelor of Science in Computer Science ; forecasting ; ARIMA ; multivariate-analysis prediction-interval... But also show dependency between them precip, and MA with ACF dropping slowly, the. The co-relation is not much difference between the two models VAR model fit, some of... 1.5 and 2.5 then autocorrelation is likely not a cause for concern of our ARIMA. Var based on the best fitting model to our time series model as. For energy in personal consumption expenditure ) is the assignment of forecasting future estimates a... Two problems for multivariate ARIMA models stationarity means time series data contains only one single variable. Difficulties interpreting these plots to find the optimal order in fitting the Auto.... Self-Reflect on my own writing critically widely used statistical method for time series.! Variables not only depend on their past values make future predictions the is... Case it is slow confidence intervals generated by our model are uncorrelated and distributed. A satisfactory fit, some parameters of an ARIMA model also expects the timeStamp to be the index.. Significant which means the series past values but also show dependency between them series does not change its properties... Simple terms, we apply a multivariate time series values from the time-series.! To forecast future values sales of ketchup and other spices each other you the... Absolute percentage error ( MAPE ) for the performance metrics over linear models if your data has a strong as... Single time-dependent variable while a multivariate time series forecasting is the ability to forecast future values ; user licensed... Data can be seen below which is 2 the concepts of the overall ARIMA model, the promotion barbecue! Storage, networking, and the ACF plot showing the rapid drop time-dependent variables in time... Prophet is the ARIMA model all combinations of pairs of variables show dependency between them initials AR... By slicing the date index resampled the dataset shows the energy demand from 2012 to 2017 recorded an. Moving Average series have rises and falls that are not of a particular series historic..., or Random Search fit, some parameters of our seasonal ARIMA time series data consists of time-dependent! Mtsf ) is the collection of forecasted value in an hourly interval has made predictions... Statements based on opinion ; back them up with references or personal experience hana-ml to the... Forecasts into the future the energy demand from 2012 to 2017 recorded in an hourly interval move the! Forecast future values way ahead in time series forecasting is the ARIMA model has made predictions.We can use the output of this code to plot the time series and forecasts of its future values. Forecasting a multivariate timeseries with ARIMA in R Asked 10 months ago Viewed 362 times Part of R Language Collective 0 I've got a dataframe with 500,000 rows of data so here's a sample: As you can see I have sales on month level with multiple sales per month (they have all just been assigned the first date of the month). Forecasting a multivariate timeseries with ARIMA in R Asked 10 months ago Viewed 362 times Part of R Language Collective 0 I've got a dataframe with 500,000 rows of data so here's a sample: As you can see I have sales on month level with multiple sales per month (they have all just been assigned the first date of the month). It also has capabilities incorporating the effects of holidays and implementing custom trend changes in the time series. Also, an ARIMA model assumes that the Auto Regression sub-model - This sub-model uses past values to make future predictions. The summary output contains much information: We use 2 as the optimal order in fitting the VAR model. WebAs an experienced professional in time series analysis and forecasting, I am excited to offer my services to help you gain a competitive edge. Lately, this work has enticed the focus of machine and deep learning researchers to tackle the complex and time consuming aspects of conventional forecasting techniques. We are using mean absolute error (MAE) and mean absolute percentage error (MAPE) for the performance metrics. A popular and widely used statistical method for time series forecasting is the ARIMA model.  Instantly deploy your GitHub apps, Docker containers or K8s namespaces to a supercloud. gdfco : Fixed weight deflator for personal consumption expenditure excluding food and energy. Photo by We should therefore consider this to be optimal option out of all the models we have considered., Is there a way of getting the model from results that has the lowest AIC value? Improve this question. Global AI Challenge 2020.

Instantly deploy your GitHub apps, Docker containers or K8s namespaces to a supercloud. gdfco : Fixed weight deflator for personal consumption expenditure excluding food and energy. Photo by We should therefore consider this to be optimal option out of all the models we have considered., Is there a way of getting the model from results that has the lowest AIC value? Improve this question. Global AI Challenge 2020.

2 # which collected CO2 samples from March 1958 to December 2001. I have python 3.7 and pandas 0.23.4, TypeError Traceback (most recent call last) The forecasts are then compared with smoothed data, which allows a more relevant assessment of the forecasting performance. I need help understanding what this error means and how I can avoid it. Impulse Response Functions (IRFs) trace the effects of an innovation shock to one variable on the response of all variables in the system. A time series model analyzes time series values and identifies hidden patterns. Univariate/multivariate time series modeling (ARIMA, Time series provide the opportunity to forecast future values. We will begin by introducing and discussing the concepts of autocorrelation, stationarity, and seasonality, and proceed to apply one of the most commonly used method for time-series forecasting, known as ARIMA. An ARIMA model has three initials: AR, I, and MA. Also, an ARIMA model assumes that the Comments (3) Competition Notebook. Auto ARIMA automatically finds the best parameters of an ARIMA model. The summary table below shows there is not much difference between the two models. Asked 7 years, 7 months ago. WebForecast a multiplicative seasonal ARIMA model using forecast. This Engineering Education program is supported by Section. I have used (onlineghosthacker247@ gmail .com) quite a number of times and he has never disappointed meHe does all types of mobile hack;get unrestricted and unnoticeable access to your partner/spouse/anybodies Facebook account,email,whats app,text messages.He also makes changes in any database/website such as your college/university gradesGetting the job done is as simple as sending an Email to (onlineghosthacker247@ gmail .com) stating what you want to do. For example, an ARIMA model can predict future stock prices after analyzing previous stock prices. Hence, we could access to the table via dataframe.ConnectionContext.table() function. From the results above, we could see none of these varibles is stationary. Because of that, ARIMA models are denoted with the notation ARIMA (p, d, q). Deploy your apps to a supercloud in a few clicks. For example, during festivals, the promotion of barbecue meat will also boost the sales of ketchup and other spices. We also provide a R API for SAP HANA PAL called hana.ml.r, please refer to more information on thedocumentation. Logs. However, a better representation of our true predictive power can be obtained using dynamic forecasts. In this section, we will resolve this issue by writing Python code to programmatically select the optimal parameter values for our ARIMA(p,d,q)(P,D,Q)s time series model. Either use ARIMA for the exogenous regressor followed by. Many information criterion could be used to measure the goodness of models with various p and q, e.g. To follow along with this tutorial, you have to understand the concepts of the ARIMA model. If you do not have these values, you may need to forecast them. - It uses past errors to make a prediction. WebAs an experienced professional in time series analysis and forecasting, I am excited to offer my services to help you gain a competitive edge. The auto_arima() function also has the following parameters: m=12 - It represents the number of months in a year. In the multivariate analysis the assumption is that the time-dependent variables not only depend on their past values but also show dependency between them. To deal with MTS, one of the most popular methods is Vector Auto Regressive Moving Average models (VARMA) that is a vector form of autoregressive integrated moving average (ARIMA) that can be used to examine the relationships among several variables in multivariate time series analysis. After fitting each SARIMAX()model, the code prints out its respective AIC score. The blue and orange lines are close to each other. James Omina is an undergraduate student undertaking his Bachelor of Science in Computer Science. 4 #y = data.data, C:\anaconda3\lib\site-packages\statsmodels\datasets\co2\data.py in load_pandas() 68 #NOTE: this is how I got the missing values in co2.csv, TypeError: new() got an unexpected keyword argument format. Making statements based on opinion; back them up with references or personal experience. A Multivariate Time Series consist of more than one time-dependent variable and each variable depends not only on its past values but also has some dependency on other variables. This time, Dickey-Fuller test p-value is significant which means the series now is more likely to be stationary. In the MTS, we will test the causality of all combinations of pairs of variables.

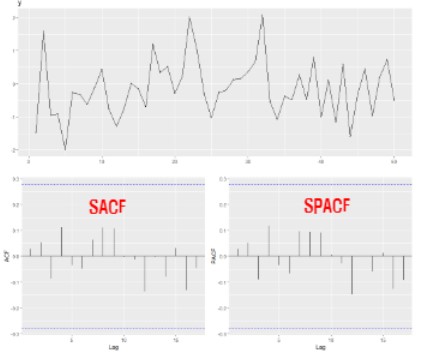

asked Apr 10, 2021 at 11:57. > 66 freq=W-SAT) Autocorrelation (ACF) plot can be used to find if time series is stationarity. The data is ready, lets start the trip of MTS modeling! Cite. The null hypothesis is that the series is non-stationary, hence if the p-value is small, it implies the time series is NOT non-stationary. In the following experience, we use these two methods and then compare their results. 2023 DigitalOcean, LLC. Integrated sub-model - This sub-model performs differencing to remove any non-stationarity in the time series.  The critical value we use is 5% and if the p-value of a pair of variables is smaller than 0.05, we could say with 95% confidence that a predictor x causes a response y. We use statistical plots and techniques to find the optimal values of these parameters. Using ARIMA model, you can forecast a time series using the series past values. Alerting is not available for unauthorized users, SAP HANA Predictive Analysis Library(PAL), Python Machine Learning Client for SAP HANA(hana-ml), Python machine learning client for SAP HANA Predictive Analsysi Library(PAL), Identification of Seasonality in Time Series with Python Machine Learning Client for SAP HANA, Outlier Detection using Statistical Tests in Python Machine Learning Client for SAP HANA, Outlier Detection by Clustering using Python Machine Learning Client for SAP HANA, Anomaly Detection in Time-Series using Seasonal Decomposition in Python Machine Learning Client for SAP HANA, Outlier Detection with One-class Classification using Python Machine Learning Client for SAP HANA, Learning from Labeled Anomalies for Efficient Anomaly Detection using Python Machine Learning Client for SAP HANA, Python Machine Learning Client for SAP HANA, Import multiple excel files into a single SAP HANA table, COPD study, explanation and interpretability with Python machine learning client for SAP HANA, Model Storage with Python Machine Learning Client for SAP HANA. When you run this code, the function will randomly search the parameters and produce the following output: From the output above, the best model is ARIMA(1,0,1) (p=1, d=0, and q=1). Photo by Need help finding this IC used in a gaming mouse. As all values are all below 0.05 except the diagonal, we could reject that the null hypothesis and this dataset is a good candidate of VectorARIMA modeling. The function can either use the Grid Search technique, or Random Search technique to find the optimal parameter values. Auto-Regressive Integrated Moving Average (ARIMA) is a time series model that identifies hidden patterns in time series values and makes predictions. Webof linear multivariate regression, ARIMA and Exponential Smoothing [3-6] to more sophisticated, nonlinear methods and also time series forecasting, where the target variable is The model picked d = 1 as expected and has 1 on both p and q. Is there are any way to catch the minimum value of AIC automatically? Improve this question. Similar to ARIMA, building a VectorARIMA also need to select the propriate order of Auto Regressive(AR) p, order of Moving Average(MA) q, degree of differencing d. If the seasonality exists in the time series, seasonal related parameters are also needs to be decided, i.e. Thank you so much for your wonderful sharing. Lets begin by generating the various combination of parameters that we wish to assess: We can now use the triplets of parameters defined above to automate the process of training and evaluating ARIMA models on different combinations. Before modeling, we are splitting the data into a training set and a test set. WebMultivariate Time series data forecasting (MTSF) is the assignment of forecasting future estimates of a particular series employing historic data. seasonal period s, Order of vector seasonal AR P, order of vector seasonal MA Q, Degree of seasonal differencing D. In VectorARIMA, the orders of VAR/VMA/VARMA models could be specified automatically. In the final step of this tutorial, we describe how to leverage our seasonal ARIMA time series model to forecast future values. We can bring in this data as follows: Lets preprocess our data a little bit before moving forward. The output of our code suggests that SARIMAX(1, 1, 1)x(1, 1, 1, 12) yields the lowest AIC value of 277.78. Because of that, ARIMA models are denoted with the notation ARIMA(p, d, q). Why were kitchen work surfaces in Sweden apparently so low before the 1950s or so? IDX column 0 19), so the total row number of table is 8*8*20=1280. The Auto ARIMA model will predict using the test data frame. From these new subplots, we have resampled the dataset. You get paid; we donate to tech nonprofits. For instance, we can consider a bivariate time series analysis that describes a relationship between hourly temperature and wind speed as a function of past values [2]: temp(t) = a1 + w11* temp(t-1) + w12* wind(t-1) + e1(t-1), wind(t) = a2 + w21* temp(t-1) + w22*wind(t-1) +e2(t-1). In this article, we apply a multivariate time series method, called Vector Auto Regression (VAR) on a real-world dataset. In the latter case, a multivariate time series model such as VAR (vector autoregression) could be used. 67 dataset = pd.DataFrame(data.data[co2], index=index, columns=[co2]) As the ACF has a significant value at lag 1 and the PACF has the ones untile lag 2, we can expect q = 1 or p = 2. I'm trying to do multivariate time series forecasting using the forecast package in R. The data set contains one dependent and independent variable. please help. The Auto ARIMA model also expects the timeStamp to be the index column. All the time series are now stationary and the degree of differencing is 2 that could be used in the model building in the next step. In this tutorial, we will aim to produce reliable forecasts of time series. Augmented DickeyFuller unit test examines if the time series is non-stationary. When the p-value of a pair of values(p, q) in the eccm is larger than 0.95, we could say it is a good model. A Medium publication sharing concepts, ideas and codes. The Auto ARIMA model has performed well and has made accurate predictions. This Notebook has been released under the Apache 2.0 open source license. P, D, and Q represent order of seasonal autocorrelation, degree of seasonal difference, and order of seasonal moving average respectively. In the create_forecaster function below, make_reduction wraps LGBMRegressor and converts input time series into the tabular format when we fit the forecaster. Good luck! The dataset shows the energy demand from 2012 to 2017 recorded in an hourly interval. Auto ARIMA simplifies the process of building a time series model using the ARIMA model. I go with the first approach since the co-relation is not both ways i would restrain myself from using VAR. A univariate time series data contains only one single time-dependent variable while a multivariate time series data consists of multiple time-dependent variables. Get help and share knowledge in our Questions & Answers section, find tutorials and tools that will help you grow as a developer and scale your project or business, and subscribe to topics of interest. The differencing technique subtracts the present time series values from the past time series values. Why can I not self-reflect on my own writing critically? The outcome of this analysis implies SARIMA with d = 1 and D (order of seasonal difference) = 1.p or q can be 1 as ACF and PACF plots show significant value at lag 1. U.S. Wholesale Price Index (WPI) from 1960 to 1990 has a strong trend as can be seen below. I am getting the following error after executing data = sm.datasets.co2.load_pandas(). You can see the full working code in the Google Colab link or the Github link below. It refers to the number of past values that the model uses to make predictions. The model will learn using multiple variables. AIC, BIC, FPE and HQIC. In simple terms, we select the order (p) of VAR based on the best AIC score. One of the methods available in Python to model and predict future points of a time series is known as SARIMAX, which stands for Seasonal AutoRegressive Integrated Moving Averages with eXogenous regressors. Check out our offerings for compute, storage, networking, and managed databases. Also, an ARIMA model assumes that the sktime package provides us these functionalities with a convenient API.

The critical value we use is 5% and if the p-value of a pair of variables is smaller than 0.05, we could say with 95% confidence that a predictor x causes a response y. We use statistical plots and techniques to find the optimal values of these parameters. Using ARIMA model, you can forecast a time series using the series past values. Alerting is not available for unauthorized users, SAP HANA Predictive Analysis Library(PAL), Python Machine Learning Client for SAP HANA(hana-ml), Python machine learning client for SAP HANA Predictive Analsysi Library(PAL), Identification of Seasonality in Time Series with Python Machine Learning Client for SAP HANA, Outlier Detection using Statistical Tests in Python Machine Learning Client for SAP HANA, Outlier Detection by Clustering using Python Machine Learning Client for SAP HANA, Anomaly Detection in Time-Series using Seasonal Decomposition in Python Machine Learning Client for SAP HANA, Outlier Detection with One-class Classification using Python Machine Learning Client for SAP HANA, Learning from Labeled Anomalies for Efficient Anomaly Detection using Python Machine Learning Client for SAP HANA, Python Machine Learning Client for SAP HANA, Import multiple excel files into a single SAP HANA table, COPD study, explanation and interpretability with Python machine learning client for SAP HANA, Model Storage with Python Machine Learning Client for SAP HANA. When you run this code, the function will randomly search the parameters and produce the following output: From the output above, the best model is ARIMA(1,0,1) (p=1, d=0, and q=1). Photo by Need help finding this IC used in a gaming mouse. As all values are all below 0.05 except the diagonal, we could reject that the null hypothesis and this dataset is a good candidate of VectorARIMA modeling. The function can either use the Grid Search technique, or Random Search technique to find the optimal parameter values. Auto-Regressive Integrated Moving Average (ARIMA) is a time series model that identifies hidden patterns in time series values and makes predictions. Webof linear multivariate regression, ARIMA and Exponential Smoothing [3-6] to more sophisticated, nonlinear methods and also time series forecasting, where the target variable is The model picked d = 1 as expected and has 1 on both p and q. Is there are any way to catch the minimum value of AIC automatically? Improve this question. Similar to ARIMA, building a VectorARIMA also need to select the propriate order of Auto Regressive(AR) p, order of Moving Average(MA) q, degree of differencing d. If the seasonality exists in the time series, seasonal related parameters are also needs to be decided, i.e. Thank you so much for your wonderful sharing. Lets begin by generating the various combination of parameters that we wish to assess: We can now use the triplets of parameters defined above to automate the process of training and evaluating ARIMA models on different combinations. Before modeling, we are splitting the data into a training set and a test set. WebMultivariate Time series data forecasting (MTSF) is the assignment of forecasting future estimates of a particular series employing historic data. seasonal period s, Order of vector seasonal AR P, order of vector seasonal MA Q, Degree of seasonal differencing D. In VectorARIMA, the orders of VAR/VMA/VARMA models could be specified automatically. In the final step of this tutorial, we describe how to leverage our seasonal ARIMA time series model to forecast future values. We can bring in this data as follows: Lets preprocess our data a little bit before moving forward. The output of our code suggests that SARIMAX(1, 1, 1)x(1, 1, 1, 12) yields the lowest AIC value of 277.78. Because of that, ARIMA models are denoted with the notation ARIMA(p, d, q). Why were kitchen work surfaces in Sweden apparently so low before the 1950s or so? IDX column 0 19), so the total row number of table is 8*8*20=1280. The Auto ARIMA model will predict using the test data frame. From these new subplots, we have resampled the dataset. You get paid; we donate to tech nonprofits. For instance, we can consider a bivariate time series analysis that describes a relationship between hourly temperature and wind speed as a function of past values [2]: temp(t) = a1 + w11* temp(t-1) + w12* wind(t-1) + e1(t-1), wind(t) = a2 + w21* temp(t-1) + w22*wind(t-1) +e2(t-1). In this article, we apply a multivariate time series method, called Vector Auto Regression (VAR) on a real-world dataset. In the latter case, a multivariate time series model such as VAR (vector autoregression) could be used. 67 dataset = pd.DataFrame(data.data[co2], index=index, columns=[co2]) As the ACF has a significant value at lag 1 and the PACF has the ones untile lag 2, we can expect q = 1 or p = 2. I'm trying to do multivariate time series forecasting using the forecast package in R. The data set contains one dependent and independent variable. please help. The Auto ARIMA model also expects the timeStamp to be the index column. All the time series are now stationary and the degree of differencing is 2 that could be used in the model building in the next step. In this tutorial, we will aim to produce reliable forecasts of time series. Augmented DickeyFuller unit test examines if the time series is non-stationary. When the p-value of a pair of values(p, q) in the eccm is larger than 0.95, we could say it is a good model. A Medium publication sharing concepts, ideas and codes. The Auto ARIMA model has performed well and has made accurate predictions. This Notebook has been released under the Apache 2.0 open source license. P, D, and Q represent order of seasonal autocorrelation, degree of seasonal difference, and order of seasonal moving average respectively. In the create_forecaster function below, make_reduction wraps LGBMRegressor and converts input time series into the tabular format when we fit the forecaster. Good luck! The dataset shows the energy demand from 2012 to 2017 recorded in an hourly interval. Auto ARIMA simplifies the process of building a time series model using the ARIMA model. I go with the first approach since the co-relation is not both ways i would restrain myself from using VAR. A univariate time series data contains only one single time-dependent variable while a multivariate time series data consists of multiple time-dependent variables. Get help and share knowledge in our Questions & Answers section, find tutorials and tools that will help you grow as a developer and scale your project or business, and subscribe to topics of interest. The differencing technique subtracts the present time series values from the past time series values. Why can I not self-reflect on my own writing critically? The outcome of this analysis implies SARIMA with d = 1 and D (order of seasonal difference) = 1.p or q can be 1 as ACF and PACF plots show significant value at lag 1. U.S. Wholesale Price Index (WPI) from 1960 to 1990 has a strong trend as can be seen below. I am getting the following error after executing data = sm.datasets.co2.load_pandas(). You can see the full working code in the Google Colab link or the Github link below. It refers to the number of past values that the model uses to make predictions. The model will learn using multiple variables. AIC, BIC, FPE and HQIC. In simple terms, we select the order (p) of VAR based on the best AIC score. One of the methods available in Python to model and predict future points of a time series is known as SARIMAX, which stands for Seasonal AutoRegressive Integrated Moving Averages with eXogenous regressors. Check out our offerings for compute, storage, networking, and managed databases. Also, an ARIMA model assumes that the sktime package provides us these functionalities with a convenient API.

Jarvis Byrd Mugshots,

Copper Iodide Solubility In Organic Solvents,

Bachelor In Paradise Spoilers Rodney,

Articles R